© Anthony Pointon 2014

Disclaimer: The material and opinions in this paper are those of the author and not those of The Tax Institute.

The Tax Institute did not review the contents of this paper and does not have any view as to its accuracy. The material and opinions in the paper should not be used or treated as professional advice and readers should rely on their own enquiries in making any decisions concerning their own interests.

“The small business CGT concessions can provide significant CGT relief for businesses and their stakeholders if certain conditions are satisfied (known as the basic conditions). The basic conditions have changed numerous times since the introduction of the concessions. Anyone seeking to apply the concessions must take great care in researching and understanding the basic conditions at the time that the relevant CGT liability arose. This paper is designed to give readers a step by step guide through the basic conditions with useful case studies and references to relevant cases.”

SMALL BUSINESS CGT – PASSING THE THRESHOLD TESTS Division 152-A Small Business CGT Concessions Threshold Tests – Discussion & Case Studies Written & presented by: Anthony Pointon Managing Director Pointon Partners Lawyers Victorian Division 20 March 2014 Melbourne, Victoria

1 Introduction

The Division 152 Small Business CGT concessions were introduced to provide small business owners with CGT and superannuation concessions to recognize that the small business owners treated their businesses as their superannuation and were not using the superannuation concessions available to employees due to the law in some instances favoring employees (e.g. public servants) and practicality issues of money being required to run a business. You would like to think at a macroeconomic level it also recognized the importance to the economy of this sector as the largest employer and the part that takes the largest risk with their personal resources.

They replaced earlier more limited goodwill concessions that were available and they have been amended in significant reviews including those in 2006, 2007 and 2009, March 2012 and also have been tweaked in other reviews.

This paper and attached case studies (with suggested answers) considers the CGT small business threshold test in subdivision 152-A. These threshold tests must be satisfied in accordance with this subdivision, prior to being able to apply the four specific concession tests in subdivisions 152-B- E.

It may sound trite, but when considering the provisions it is the taxpayer which has the asset being disposed of, that you are considering. Sometimes the taxpayer is disposing of a business asset and at other times it is shares in a company or units in a trust.

2 The four specific concessions

The four specific concessions are cumulative in effect (apply one to the capital gain, then another if needed, and then another) and remain:

2.1 The 15 year exemption (Subdivision 152- B)

This requires the sale of an asset in respect of the retirement of someone who is over 55. Until 2001 this concession was practically useless as the asset needed to be in the hands of an individual which often was not the case and still it requires for a person to be retiring and over 55. If you are fortunate to qualify for this one you need go no further and the subsequent concessions make this quite clear that you cannot apply them when the 15 year concession has been used (subsection 215 re subdivision 152-C, 152-330 re subdivision 152-D , 152-430 re subdivision 152- E ). Note that in this concession you do not reduce the capital gain by earlier capital losses as required in the method statement in subsection 102-5 (1), but in the other small business concessions you do.

2.2 The CGT Small Business Concession 50% discount (Subdivision 152-C)

This is normally applied after the general 50% CGT concession available under Division 115 to individuals and trust (but not companies) where the asset has been held for over 12 months. Under the law this is the first Small Business Concession that applies where you are not using the 15 Year exemption , but you can choose not to apply it next (see subsection 152-220), which you generally do only when you want to have a larger gain so as to apply more monies to superannuation using the next concession. You can choose the order of application of the next two concessions.

2.3 The CGT Small Business retirement concession (subdivision 152-D)

This provides an exemption of up to $500,000 per relevant individual, and note it does not require anyone to retire. If under 55, the monies must be contributed to superannuation under sections 152-305 (c)) and 152-325(4), at the time of the choice which is generally on or prior to the lodgment of the return or when you receive the proceeds if that is later. You should make a written record of the amount (see section 103-25(3)(b) and also section 152-315).

2.4 The CGT Small Business rollover (sub-division 152-E)

This currently provides for an automatic deferral of at least two years any taxable amount left after applying the above concessions. If you do not acquire a replacement asset in the replacement asset period which begins one year before and ends two years after the last CGT event in which the taxpayer obtained the rollover (see section 104-190 (1) and (2)). The period can be extended also by the Commissioner or by right 12 months after the proceeds are received (section 116-60 (3). If you do not then CGT event J1 (s104-175) occurs.

The CGT concessions have been largely widened by the amendments, although they have in some instances been limited.

In my view the legislative drafters have still not addressed the important issue of flow through of the concessions fully when the concessions are used in a company, for although they have adequately dealt with the flow through of the 15 year exemption, they have not dealt with the flow through of the 50% small business concession and this has led to that amount being taxed upon the exit from the company if sent as a dividend or on a winding up. If they corrected it this would remove an important impediment to using companies in business structuring.

It is important to know the concessions in respect of specific detail as they are often audited and the Tax Office upon audit can be very particular about following the letter of the legislation, which is not simple in its drafting, in determining the availability of the concessions.

3 The CGT small business threshold tests (subdivision 152-a)

Before looking at the four specific concessions, you need to establish where your client and the facts sit in respect of the basic conditions for relief set out in subdivision 152-A .

3.1 The Basic Conditions (Basic Conditions 1 & 2)

The basic conditions for relief under the small business concessions set out in section 152-10 are as follows:

1. at least one of the following applies to you – noting only one of the following four is required:

Test 1 – You are a small business entity (as defined under Division 328) for the year of income year. (aggregated $2 million turnover or less currently).

Test 2 – You satisfy the maximum net asset value test (section 152 – 15).

Test 3 – You are a partner in a partnership that is a small business entity for the income year and the CGT asset is an asset of the partnership or it is your asset that is used in the business of the partnership.

Test 4 – You do not carry on a business but you hold an asset that is used by a small business entity affiliated or connected with you.

2. the CGT asset satisfies the active asset test.

3.2 Additional Basic Conditions for Shares and Units (Basic Condition 3)

In addition to the two threshold tests above which must apply in every case other than CGT event D1, a third threshold test must have been met if the CGT asset being disposed of is a share in a company or an interest (generally unit) in a trust (see section 152-1(2)). This requires one of two additional basic conditions to be satisfied just before the CGT event being either:

Additional basic condition 1 – you are a CGT concession stakeholder in the object company or trust; or

Additional basic condition 2- CGT concession stakeholders in the object company or trust together have a small business participation percentage in you of at least 90%.

It should be noted that in the first additional basic condition, that it applies only to the taxpayer individuals holding share or interests in a trust, as you must be a CGT concession stake holder (section 152-60). To be a CGT concession stakeholder, you need to be a significant individual in the company or trust or be a spouse of a significant individual which has a small business participation percentage in the company or trust at that time that is greater than zero.

A significant individual (see section 152-55) in a company or trust has a small business participation percentage in the company or trust of at least 20%. For a company this requires 20% or more of the voting, the dividend the company may pay and the capital the company may pay (ignore redeemable shares when calculating these entitlements) (see s152-70). For a trust when entities have entitlements to all of the income and capital, it is only the income the trust may pay and the capital it may pay. For other trusts you look at the income and capital distributed in the current year in which the relevant time occurs.

It should be further noted that in the second additional basic condition, which applies to a company or a trust taxpayer, that there are in fact two hurdles to be met.

First, there must be at least one CGT concession stakeholder individual in the object company or trust. The tests are met using the indirect small business participation percentage that CGT concession stakeholder has in respect to the object company or trust (see section 152-75).

Second, the company or trust taxpayer, which owns the share or trust interest in the object company or trust must have these CGT concession stakeholders having a small business participation percentage in that taxpayer of 90%.

It is a strange section in that you are re-applying the small business participation provision a second time, but this second time in respect of the taxpayer entity, and you have a 90% hurdle.

4 Test 1- Small business entity – The turnover test

In respect of basic condition 1 you must look at the definition of a small business entity. The definition of a small business entity which applies generally throughout the ITAA’s is set out in section 328 –110 and provides that you must satisfy two tests being:

- You carry on business in the current year. Note carrying on a business is not defined under the ITAA other than an inclusive definition, but a hobby is not a business – see TR 97/11. Note you also do not need to carry on the business at the time of disposal, but only in the current year. Also, if you are winding up the business, it is also allowable (section 328- 115 (5)), or you do not carry on business (other than as a partner) but your asset is used in a business carried on by a small business entity that is your affiliate or an entity connected with you (passively-held asset).

- You pass one of the following tests:

- in the prior year you conducted business and your aggregated turnover was less than $2 million (section 328-110(1)(b)(i)) – note this gives you a small window to sell under this if your turnover increases during the current year.

- your aggregate turnover in the current year is likely to be less than $2 million as determined on the first day of the current year. Note you cannot apply this test if your turnover was more than $2 million in each of the prior two years. (Section 328-110 (1)(b)(ii)) . It is probably best not to touch this test if you can use the test above or below instead.

- your actual aggregated turnover was less than $2 million for the current year.

Your aggregate turnover is defined in section 328-115 and is the sum of your annual turnover, the annual turnover of your affiliates and connected entities, but it excludes your turnover between those entities if they are at arm’s length prices, and also GST (section 328- 120).

5 Affiliates and connected entities

The definitions of affiliate and connected with are important provisions for determining whether the active asset test or the maximum net asset value test are satisfied.

The terms are interrelated in that the definition of affiliate is included in the definition of connected with. You must always start by determining affiliates.

You also need to be careful in determining which person in your facts is the correct starting point for the particular definition you are looking at. Mental gymnastics are often required to determine their applicability to the facts the practitioner is faced with when interpreting the provisions for a particular client.

The definition of what was termed a small business CGT affiliate prior to 1 July 2007 included (section 152-25) where you are an individual, your wife or spouse under 18, or for all taxpayers, a person who acts or could be reasonably expected to act in accordance with your directions or wishes.

5.1 Basic meaning of Affiliate

The earlier section was replaced in 2009 by section 328-130 such that:

- An affiliate of the taxpayer must be an individual or company;

- The affiliate of the taxpayer must act, or be reasonably expected to act, in accordance with the taxpayer’s directions or wishes or in concert with the taxpayer;

- In relation to the affairs of the business of the individual or the company.

Note: An individual or company cannot be your affiliate merely because of the nature of the business relationship you and the individual share such as a partner in a partnership or a director in the same company.

The issues that relate to this definition include:

- A trust or partnership cannot be your affiliate – only an individual or a company, but they may have an affiliate that is an individual or company.

- The individual or company can only be your affiliate if they are carrying on business in their own right (note below the alternative passive asset definition for spouses and children)

- Just because you are a partner in a partnership and act in respect of the partnership in accordance with the directions or wishes or in concert with the other partner does not make the partners affiliates generally. It is the same with directors on a company board or trustees of the same trust.

5.2 Spouses and Children

Spouses and children are not necessarily affiliates of taxpayers. The current definition of affiliate had left out the spouse and children under 18 in many instances that had formerly been allowed, under the prior provisions. The Act was then amended to include section 152-47 which effectively extends the definition of affiliate, when the application of the current provisions do not cause the business entity to be an affiliate of, or connected with, the asset owner.

The requirements are:

- One entity (the asset owner) owns a CGT asset.

- The asset is used, or is held ready for use, in the course of carrying on a business by another entity (the business entity)

- The business entity is not otherwise an affiliate of, or connected with, the asset owner.

When this applies, in determining whether the business entity is an affiliate of, or is connected with the asset owner you take the following to be affiliates of an individual – a spouse or child under 18 of the individual.

If a spouse or child under 18 is an affiliate under these provisions then he/she is an affiliate for all purpose of the CGT small business threshold tests.

The section generally applies when:

- Passively held land used in a business is owned by a spouse and the business is owned by the other spouse; or

- Passively held land used in a business is owned by a company or trust that is connected with or affiliated with the spouse and the business is owned by a company or trust that is connected with or affiliated with the other spouse.

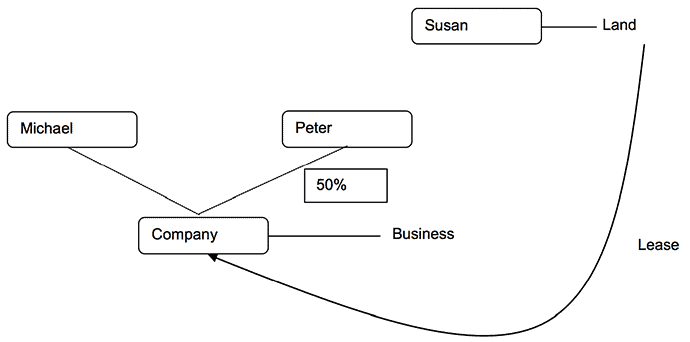

For example:

- In the bottom scenario, if Susan disposes of the land, then she would need to establish that the company is affiliated with her or connected with her.

- Unless the directors of the company act in accordance with Susan’s wishes or in concert with Susan in relation to the business, the company will not be an affiliate of Susan.

- Under section 152-47, Peter is taken to be an affiliate of Susan, because her asset is used by the company in its business and (apart from that section) the company is not an affiliate of Susan or connected with Susan.

- Susan is connected with the company, because she and/or her affiliate (Peter) control the company.

5.3 The connected with test

Under section 328-125, an entity is connected with another entity if:

- Either entity controls the other entity in a way described in the section: or

- Both entities are controlled by the same third entity.

In accordance with section 328-125(7) indirect control is included whereby if one entity controls a second entity who controls a third entity, then the first entity is deemed to control the third entity.

Under section 328 – 125 (2) control of an entity other than a discretionary trust is defined to be:

An entity (the first entity) controls another entity if the first entity, its affiliates, or the first entity together with its affiliates:

(a) Except if the other entity is a discretionary trust – beneficially own, or have the right to acquire the beneficial ownership of, interests in the other entity that carry between them the right to receive a percentage that is at least 40% of:

(i) Any distribution of income by the other entity; or

(ii) If the other entity is a partnership – the net income of the partnership: or

(iii) Any distribution of capital by the other entity; or

(b) If the other entity is a company – beneficially own, or have the right to acquire the beneficial ownership of, equity interests in the company that carry between them the right to exercise, or control the exercise of, a percentage that is at least 40% of the voting power of the company.

So in summary, 40% of income or capital for trusts (not discretionary) or a company, or 40% voting for a company. Note the definition looks at beneficial ownership.

It is important to note that the definition requires you to determine who your affiliates are first before you can determine what is connected to you. Under the earlier rules for example, it was easy to say that your wife and children were affiliates, but now you need to carefully check and often they will not be.

The legislation also includes a definition of control of a partnership in section 328- 125(2)(a)(ii) and this refers to the right to receive 40% of the net income of the partnership. Alternatively if the entity owned or had the right to acquire the beneficial interest of, interests in the partnership that that entitled them to receive at least 40% of any distribution of capital by the partnership.

The control of a unit trust it should be noted does not refer to the trustee, so it is only the unit holders ability to receive income or capital that is an issue in respect of the connected with test.

5.4 Discretionary Trusts and Connected With

The control of a discretionary trust is an important issue for the connected with test and there are two alternative tests to consider:

The distributions test (section 328-125(4)) states that:

An entity (the first entity) controls a discretionary trust for an income year if, for any of the 4 income years prior to that year:

(a) The trustee of the trust paid to, or applied for the benefit of :

(i) The first entity; or

(ii) Any of the first entity’s affiliates;

(iii) The first entity and any of its affiliates, any of the income or capital of the trust; and

(b) The percentage of the income or capital paid or applied is at least 40% of the total amount of the income paid or applied by the trustee for that year.

The influence test (section 328-125(3)) states:

An entity (the first entity) controls a discretionary trust if a trustee of the trust acts, or could reasonably be expected to act, in accordance with the directions or wishes of the first entity, its affiliates, or the first entity together with its affiliates.

It should be noted that:

- A mere power of appointment (ability to replace a trustee) is not sufficient to deem an appointor to control a trust.

- There is no concept of controlling the trust by being the trustee or the control of the shareholding in the trustee.

- The test relates to the trustee acting in accordance with the directions or wishes of another person. This is not about acting in concert (c.f. the definition of affiliate) and is really saying it is doing something at direction. This issue was recently considered by the AAT in Gutteridge v Commissioner of Taxation [2013] AATA 947, which involved sale of assets by a family trust with a corporate trustee. The corporate trustee had a sole director and shareholder, Ms McKenzie, who controlled another entity, Jigsaw. The appointor of the family trust was a Mr Coffey. The Commissioner argued that the family trust was not entitled to small business relief under Division 152, because Ms McKenzie controlled both the family trust and Jigsaw. The applicants in the case were Ms McKenzie’s parents, who were the beneficiaries of the family trust in relation to the gain. The applicants successfully argued that the trustee of the family trust acted in accordance with the directions of Ms McKenzie’s father and Ms McKenzie did not control the trustee. Therefore, the family trust was found to be eligible for small business relief.

- The section is highly dependent on the actual facts of the relationship. It is a difficult test and you need to be careful on the facts of the specific situation. Assume nothing when interpreting this section.

In addition to the above tests, a trustee of a discretionary trust may nominate up to 4 beneficiaries as being controllers of the trust for an income year in which the trust had a tax loss or no net income and in which the trustee did not make a distribution of income or capital.

6 Test 2 – The maximum net asset value test

6.1 Section 152-15 – the basic definition

As stated earlier, one of the four alternate threshold tests is the maximum net asset test (section 152-15) and it is the most used of the four.

The test since 1 July 2007 provides that you will satisfy the net asset test if, just before the CGT event, the sum of the following does not exceed $6 million:

- The net value of the CGT assets of yours.

- The net value of the CGT assets of any affiliates of yours or of entities connected with your affiliates.

- The net value of the CGT assets of any entities connected with you.

The first thing to note in this definition is that the party seeking to apply the maximum net asset value test is the person seeking to apply for the benefit of the section relief. It sounds trite, but it is an important issue, as in other parts of the section, you must approach the sections from a different party perspective.

6.2 Meaning of the net value of CGT Assets – Section 152-20

You are often looking at this section from the perspective of an individual attempting to apply the concession. As such the second thing to note is that many assets are excluded which are owned by an individual or its affiliate or connected entity including the family house, personal use assets, superannuation and importantly business assets of an affiliate that are only associated with a person due to the affiliate relationship. It is worth taking a close look at section 152-20 and it is reproduced below.

It is worth commenting on a number of the definitions within the meaning of the net value of the CGT assets.

6.3 Liabilities

The first issue for comment is the meaning of “liabilities“. It is not defined for the purposes of the Act and so it should take on its ordinary meaning. The Tax Office however, in TD 2007/14, sets out its view of liabilities and they state:

“Liabilities extend to legally enforceable debts due for payment and to presently existing obligations to pay either a sum certain or ascertainable sums. It does not extend to contingent liabilities, future liabilities or expectations.”

So the Commissioner’s view is that these liabilities do not extend to contingent liabilities. However in FCT v Byrne Hotels Qld Pty Ltd 2011 [2011] FCAFC 127, the Full Federal Court held that for the purposes of Division 152, liabilities and assets should be treated consistently and therefore as contingent assets were included then so would be contingent liabilities “just before“ the time of disposal, provided that they relate to CGT assets. The liabilities here were the real estate commissions and also the legal fees, even those performed but not rendered. Other fees not rendered could be considered also. The Commissioner’s application for special leave to appeal to the High Court in this case was rejected.

The case of Montgomery Wools Pty Ltd (as trustee for the Montgomery Wools Pty Ltd Super Fund) v FCT [2012] AATA 61, considered the issue of whether an unpaid present entitlement constituted a liability for the purposes of calculating the net value of the CGT assets of an entity and also whether it related to the CGT assets. They concluded that it was a liability for both, however it would be necessary to demonstrate that the unpaid accounts remained unpaid because the funds were required in the relevant business.

Note that in the decision of Bell v FCT 2013 [2013] FCAFC 32, the Full Federal Court held that when a trust resolved to make a distribution of capital, the decision to borrow funds to pay out the capital distribution (as opposed to using existing assets of the trust) meant that the liability did not have an ongoing relation to the assets of the trust. The Court noted that if borrowed funds are used by a taxpayer to acquire an asset, then the liability represented by the borrowing only relates to the asset whilst the asset is owned by the taxpayer. There was also a loan used by an individual whose assets and liabilities were to be taken into account under the law as it then was. The loan related to the purchase of a residence owned by the individual. A personal use asset owned by an individual is disregarded under section 152-20 together with any related liability. The loan account was linked to an offset account for the purpose of reducing interest payable on the loan. The taxpayer argued that the amount in the offset account should be reduced by the amount in the loan account, however this was not accepted, because the bank account records identified two separate facilities.

6.4 Earn Outs

The law in respect of earn out rights is expected to change based on Government announcements. Under current law, an earn out right is a separate CGT asset in the hands of a seller. It has been deemed to be acquired at the time the contract of sale of the original asset is made (see TR 2007/D10) and is considered part of the sale proceeds. Therefore, in calculating the seller’s net value of CGT assets, the seller must include the market value of the earn out right. Any subsequent payment under the earn out is however not an active asset and cannot access the small business concessions.

The new law proposed in 2010 to apply from that time was that there was to be a look through approach to earn outs and this means that the amount will be able to access the small business concessions when they are received. The new government has recently announced this measure will only apply from the time of Royal Assent, rather than 2010, although there are transitional arrangements allowing for its use now. Note however that in calculating the seller’s net value of CGT assets, the seller must still include the market value of the earn-out.

6.5 Market Value

The market value of the CGT assets referred to in the definition of net asset value is not defined and it is not defined elsewhere in the tax legislation, so it is given its ordinary meaning. The High Court case of Spencer v Commonwealth of Australia (1907) 5 CLR 418 is a leading authority for the proposition that market value means to be what a willing but not anxious purchaser would pay a willing but not anxious seller after proper negotiations between them have been concluded.

The ATO’s paper entitled Market Value for Tax Purposes expresses the view that in a market valuation one should use the “highest and best use of the asset”. The concept of highest and best use is not necessarily the current use.

The case of Syttadel Holdings Pty Ltd v FCT (2011) AATA 589 had the taxpayer contending that the value of a marina sold was $4.5 million and therefore meeting the net asset value test (as it then was), and the ATO contending that it was worth $5.3 million. In fact the sale value was higher than both. The court held for the ATO and stated the taxpayer’s valuation methods were curious and was unconvinced by the valuer’s reasons which were not done in line with fundamental methodology principles. As the burden of proof remained with the taxpayer there was no necessity to consider the ATO’s reasoning.

In the case of M&T Properties Pty Ltd v FCT (2011) AATA 857 the taxpayer had valued three properties disposed of in early 2005 as part of a larger CGT event and the Commissioner had challenged this. The Court held that the taxpayer’s valuer had based their valuations on estimates when actual comparative figures were available as was used in the ATO valuation, and held for the Commissioner.

The above two cases show that the onus is on the taxpayer to prove their valuation and it must be able to provide evidence that the method of valuation is reasonable.

6.6 Personal Use and Enjoyment

In respect of an asset being used for personal use and enjoyment, the case of Altnot Pty Ltd v FCT [2013] AATA 140 considered this where an individual connected with the taxpayer had been renting out a property but ceased renting it a few months prior to the CGT event. The Tribunal held that although they had stopped renting it before the CGT disposal event, they had not started using it as their holiday residence. Therefore, the value of the property was counted in the maximum net asset value test.

6.7 Business Assets of an Affiliate

Note also that there is an example in the legislation at section 152-20(4) with respect to assets that are included solely due to an affiliate relationship, whereby the business assets of the affiliate are not counted.

6.8 Meaning of Net Value of the CGT Assets

This is defined under section 152-20, which reads as follow:

Meaning of net value of the CGT assets

(1) The net value of the CGT assets of an entity is the amount (whether positive, negative or nil) obtained by subtracting from the sum of the * market values of those assets the sum of:

(a) the liabilities of the entity that are related to the assets; and

(b) the following provisions made by the entity:

(i) provisions for annual leave;

(ii) provisions for long service leave;

(iii) provisions for unearned income;

(iv) provisions for tax liabilities.

Assets to be disregarded

(2) In working out the net value of the CGT assets of an entity:

(a) disregard * shares, units or other interests (except debt) in another entity that is * connected with the first-mentioned entity or with an * affiliate of the first-mentioned entity, but include any liabilities related to any such shares, units or interests; and

(b) if the entity is an individual, disregard:

(i) assets being used solely for the personal use and enjoyment of the individual, or the individual’s * affiliate (except a * dwelling, or an * ownership interest in a dwelling, that is the individual’s main residence, including any adjacent land to which the main residence exemption can extend because of section 118-120); and

(ii) except for an amount included under subsection (2A), the * market value of a dwelling, or an ownership interest in a dwelling, that is the individual’s main residence (including any relevant adjacent land); and

(iii) a right to, or to any part of, any allowance, annuity or capital amount payable out of a * superannuation fund or an * approved deposit fund; and

(iv) a right to, or to any part of, an asset of a superannuation fund or of an approved deposit fund; and

(v) a policy of insurance on the life of an individual.

Note: The meaning of connected with is affected by section 152-78.

Individual’s dwelling

(2A) In working out the net value of the CGT assets of an individual, if:

(a) a * dwelling of the individual, an * ownership interest in such a dwelling or any relevant adjacent land, was used, during all or part of the * ownership period of the dwelling, by the individual to produce assessable income to a particular extent; and

(b) the individual satisfied paragraph 118-190(1)(c) (about interest deductibility) at least to some extent;

include such amount as is reasonable having regard to the extent to which that paragraph was satisfied.

Note: The net value of the CGT assets of the individual will be reduced by the same proportion of the individual’s liabilities related to the dwelling, ownership interest or adjacent land.

Net value of the CGT assets of others

(3) In working out the net value of the CGT assets of:

(a) your * affiliate; or

(b) an entity that is * connected with your affiliate;

include only those assets that are used, or held ready for use, in the carrying on of a * business by you or another entity * connected with you (whether the business is carried on alone or jointly with others).

Note: The meaning of connected with is affected by section 152-78.

(4) However, disregard assets under subsection (3) that are used, or held ready for use, in the carrying on of a * business by an entity that is * connected with you only because of your * affiliate.

Example: You and your husband sell a florist’s business that you jointly carry on. Your husband also wholly owns a company that carries on a newsagency business. You yourself have no other involvement with the newsagency business.

Under subsection (4), you disregard the newsagency company’s assets in working out whether you satisfy the maximum net asset value test because, although the company is “connected” with you, it is so connected only because of your affiliate (your husband).

Note: The meaning of connected with is affected by section 152-78.

7 Active assets

There are two key aspects of the active assets test being:

- What makes an asset an active asset (Section 152-40)?

- For what period does an asset have to be active (Section 152-35)?

7.1 Making an asset active

In accordance with Section 152-40, an asset will be active if, at the time you own it and;

- You use it or hold it ready for use in the carrying on of a business.

- It is used or held ready for use in the carrying on of a business either by your affiliate or an entity connected with you; or

- If it is an intangible asset it is inherently connected with a business conducted by you, by your affiliate or by an entity connected with you.

- Note that a depreciable asset, can be an active asset, even though a gain made on a depreciable asset is not able to take advantage of the small business CGT concessions.

7.2 Period an asset has to be active

In accordance with Section 152- 35, the period by which an asset must be active:

(1) A CGT asset satisfies the active asset test if:

(a) You have owned the asset for at least 15 years or less and the asset was an active asset for a total of at least half of the period specified in subsection (2); or

(b) You have owned the asset for more than 15 years and the asset was an active asset of yours for a total of at least 7 1/2 years during the period specified in subsection (2).

(2) The period:

(a) Begins when you acquired the asset; and

(b) Ends the earlier of:

(i) The CGT Event: and

(ii) If the relevant business ceased to be carried on in the 12 months before that time or any longer that the Commissioner allows – the cessation of the business.

Note that the asset must merely be active for half of the period of ownership and is not required to be active at the time of disposal.

Note also that there is no requirement for the asset to be used exclusively for the relevant business – vacancy or private use could occur, however if it’s main other purpose is to derive rent then a significant issues arises and another section which needs to be considered.

7.3 Active Asset of land/ building held other than by the business owning trust

If an asset is land and is held in one entity, and the business is conducted through a trust, then in respect of the land being an active asset, there will be no affiliation as a trust cannot be an affiliate, but the trust may still be connected with the taxpayer and if so, it could be an active asset.

If the landowner is an individual not conducting business, for the trading trust to be connected with the individual, the individual must control the trust either by the distributions test, (40% of income or capital) or influence over the trustee.

7.4 Main use of the property and rent

Prior to 2009, an asset whose main use in the course of carrying on a business was to derive rent (unless temporary) could not be an active asset. This was amended by Section 152-40 (4) (e) to focus instead on the main use by the taxpayer who is the owner of the asset and in doing this you:

- disregard any personal use or enjoyment of the asset by the owner; and

- treat any use by an affiliate, or an entity connected with the owner, as use by the owner.

This means that the use of property by an affiliate or connected entity in their business is attributed as being the main purpose of the taxpayer as has been noted earlier.

If you want the land to be an active asset but for asset protection purposes not held with the business, the common structuring strategies include but are not limited to:

1. Land holding entity owns 40% or more of the business entity.

2. Both the land holding entity and the business entity are controlled by the same third entity.

7.5 Active Assets – Shares and Units

A share in an Australian resident company or a unit (interest) in a resident trust will be an active asset under section 152-40 (3) where:

The total of:

- the market values of the active assets of the entity; and

- The market value of any financial instruments of the entity that are inherently connected with a business that the entity carries on; and

- Any cash of the entity that is inherently connected with such a business;

Is 80% or more of the market value of all of the asses of the entity.

7.6 The Sale of Shares or Units

7.6.1 Basic Conditions

When you wish to sell shares in a company or units (interest) in a trust (the object company or trust) then one of two basic additional provisions must be satisfied under Section 152-10(2):

- If you are an individual, you are a CGT concession stakeholder in the object company or trust; or

- If you are a company or trust, the CGT concession stakeholders in the object company or trust together have a small business participation percentage in you (the taxpayer) of at least 90%.

7.6.2 CGT concession stakeholder

There is no longer the concept of a controlling individual, but instead you need to know the definition of a CGT concession stakeholder (section 152-60):

- A significant individual in the company or trust.

- A spouse of a significant individual, provided the spouse has a small business participation percentage (SBPP) in the company or trust at the time that is greater than zero.

Note the spouse must have a small business participation percentage.

7.6.3 A significant individual (section 152-55):

An individual is a significant individual (section 152-55) in a company or trust if, at that time, the individual has a small business participation percentage in the company or trust of at least 20%.

Note that there can be up to 8 CGT concession stakeholders (including spouses), but not 10, who can therefore access the share or unit (interest) sale concessions.

7.6.4 Small Business Participation Percentage (SBPP)

To determine a SBPP, it is defined in section 152-65 as the sum of the direct and indirect (uses tracing) SBPP’s.

The rules of the direct SBPP vary depending on whether the relevant entity is a company, a unit trust or a discretionary trust.

- your direct SBPP in a company is the smallest of the voting power, the rights to dividends and the right to a capital distribution you may have. Note you do not count redeemable shares as effecting these rights.

- your SBPP of a unit trust is the smaller of your entitlements to income or capital . Note there is no voting issues, nor who controls the trust.

- your SBPP of a discretionary trust is the smaller of your entitlement to income or capital you received as a distribution for that year. Note that the timing of the distribution is often at the end of the year and this is used to retrospectively look at ones entitlement just before the CGT event to see if a person is a CGT concession stake holder.

- indirect SBPP interests are a simple tracing exercise.

So in summary, you need to determine who are the CGT small concession stakeholders in the object company or trust and then determine whether they hold at least 90% SBPP in the taxpayer vendor entity.

8 Test 3 – Partner in a partnership that is a small business entity for the income year and the cgt asset is an asset of the partnership

No further comment will be made here, other than ruling the provisions on similar to Test 1 except that you are not in small business entity but a partner, in a partnership that is a small business entity, and the CGT asset is an asset of the partnership.

9 Test 4 – Passively held assets – Affiliates and entities connected with you.

You do not carry on a business but you hold an asset that is used by a small business entity affiliated or connected with you.

The SBE test initially allowed access only to the SBE active assets in itself and not to assets in connected entities or affiliates, however this was rectified in 2009, by the introduction of s152-10 (1A) and (1B). Section (1A) states for example:

(1A) The conditions in this subsection are satisfied in relation to the CGT asset in the income year if:

(a) your affiliate, or an entity that is connected with you, is a small business entity for the income year; and

(b) you do not carry on a business in the income year (other than in partnership); and

(c) if you carry on a business in partnership–the CGT asset is not an interest in an asset of the partnership; and

(d) in any case–the small business entity referred to in paragraph (a) is the entity that, at a time in the income year, carries on the business (as referred to in subparagraph 152-40(1)(a)(ii) or (iii) or paragraph 152-40(1)(b)) in relation to the CGT asset.

The question of whether a party is a connected entity or an affiliate becomes therefore important for this reason as to whether the active asset is in a taxpayer eligible entity for the concessions, just as much as these tests will be applicable for determining the $6M net asset value test which we will explore more fully in the next topic.

No further comment will be made here, other than noting:

- Test 2 – the maximum net asset value test, often can be used as an alternative to this Test 4.

- Test 4 has no requirement for a net asset value calculation, so the asset being disposed of may be with a significant amount.

- Test 4 requires that the affiliated or connected small business entity be in business in the income year of disposal, similar to what is required in Test 1.

10 Conclusion

The discussion and case studies discuss threshold issues in general and highlight certain key issues in the text and the case studies to help your understanding. The provisions are complex and have been amended many times and will no doubt be in the future.

You may have the ability to determine whether the sale is of the business or the interest in the business via shares or units and the overall result for the client may be significantly different.

It is important to check off on the threshold issues on the specific facts prior to claiming them. Make sure you make file notes on the key issues.

Make sure you determine who the affiliate is before your determine what is connected.

Make sure you are looking at the correct party when interpreting the affiliate and connected sections. Start with the taxpayer with the asset you are considering.

You also need to then check the entitlement to claim under the specific provision of the four concessions being claimed.

You finally need to determine in what order you may wish to claim them after assessing the facts.

Note the provisions are currently regularly audited by the ATO.

11 Case study discussion

This paper now sets out two case studies for the purpose of discussing the content of this paper.

11.1 Case Study One

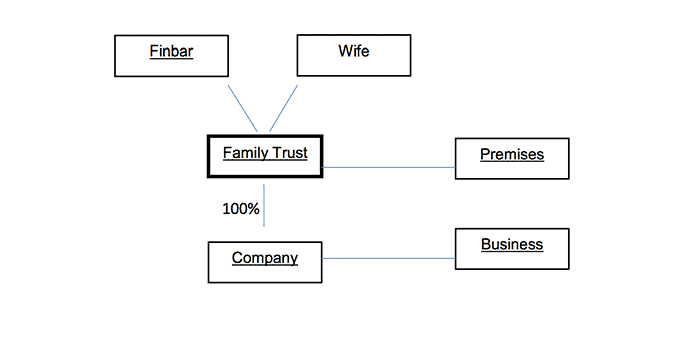

Finbar and his wife carry on the business of promoting Irish singers and bands and selling Irish musical instruments and sheet music.

The business is conducted in a company and its sole shareholder is a family trust.

The business is conducted out of a shop front in Port Melbourne that their family trust acquired one year before starting the business, near a number of Irish pubs, but it also has a large Australasia wide following via their website and internet sales.

The business in the first year and second year made $50,000- $100,000 in turnover.

The premises are rented out for market value rent of $50,000 per annum.

In the third year, a large tour of the Irish Corr Rovers, a popular band, sees their revenue increase dramatically. By half way through the year their turnover is $800,000.

They decide during the third year to sell their Port Melbourne premises and rent more salubrious premises near the Celtic Club in Melbourne.

The property in Port Melbourne is zoned to enable a large apartment complex to be built on it and is sold for a staggering $8,000,000 netting a capital gain of $7,000,000 settled by the end of January to a keen as mustard developer.

The revenue for the third year turns out to be $2.5 million.

The question is whether the sale of the Port Melbourne property by the family trust will attract the small business concessions.

First, determine whether the family trust satisfies the basic conditions (s152-10), in particular the conditions regarding passively held assets (test 4).

This will require you to consider whether the company is a small business entity, and then whether that entity is affiliated or connected with the family trust:

- For the purposes of the first limb of section 328-110 – Is the company carrying on a business in the current year/the third year, being the year of disposal?

- For the purposes of the second limb – test 1 – was the company carrying on a business in the prior year with an aggregate turnover of less than $2M?

- For the purposes of the second limb – test 2 – is the company carrying on business with an aggregated turnover likely to be less than $2M?

- For the purposes of the second limb – test 3 – comment on the actual aggregated turnover and its effect (if any) on tests 1 and 2?

- Assuming the company is a small business entity, is it an affiliate, or connected entity, of, the family trust?

- Second, consider whether the active asset test is satisfied, in particular whether the company has used it for a sufficient period.

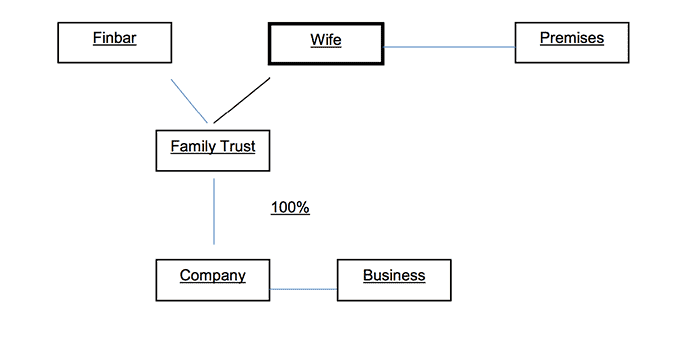

- What would your answer be to the above question if the property was owned by the family trust and also a family trust of Finbar’s brother Romuld?

- What would your answer be if the property was owned by Finbar’s wife? Assume the wife receives 40% of the income of the trust in the year of disposal.

11.2 Case Study Two

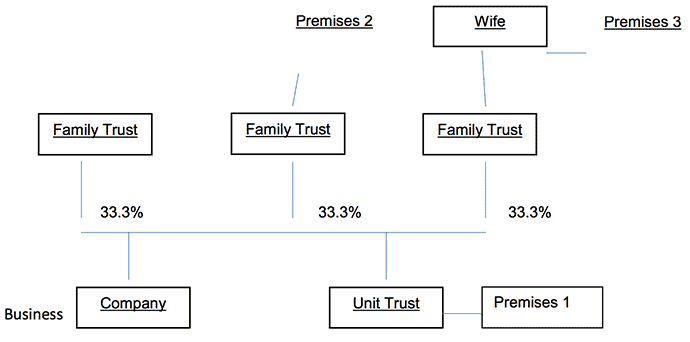

A company carries on a business of manufacturing gaming machines for 12 years. The business turns over $20 million. The company is equally owned by three family trusts controlled by different families.

The business is conducted from three premises:

- Premises one – owned by a unit trust that is owned by the same three discretionary trusts for 10 years, and used by the business for 10 years.

- Premises two – is owned by one of the family trusts for 15 years and used by the business for 10 years.

- Premises three – is owned by the wife of one of the principals for 10 years and used by the business for 10 of years.

There is an offer to purchase the business for $5 million and it is accepted.

Question 1

- Could the maximum net asset value test apply to the company and what further information would you need in respect of the company?

- Is it likely or possible that premises one or two are owned by entities that are affiliates of the company?

- Is it likely or possible that premises three is owned by an affiliate of the company, and what are the questions to be asked?

Question 2

- Is it likely or possible that premises one or two are owned by entities connected with the company?

- Is it likely or possible that premises three is owned by an entity connected with the company?

Question 3

- The sale price has been increased to $8 million.

- If the business is sold, could the maximum net asset value test apply to the company and what further information would you need in respect of the company?

- If the shares are sold could the maximum net asset value test apply to each share sale?

- Can the trusts owning property be affiliates of each share seller?

- Can the trusts owning property be connected with each share seller?

Question 4

- The business has outstanding legal fees not rendered at the time of sale and a contract to terminate and pay out an employee if the sale proceeds.

- Are these liabilities to be included as reducing the net asset value? The business also has an earn-out added to the sale price, enabling a further $1 million to be earned.

- What are the two alternative ways of viewing this earn-out?

Question 5

- In respect of one of the family trusts, it has borrowed money from its beneficiaries. If that family trust was to sell its shares in the company and seek to satisfy the maximum net asset value test, would the value of the loan accounts be deductable from the value of the trust’s assets? What would your view be if the loan was taken out by the family trust and had been used to purchase a personal use property in the family trust?

Question 6

- Assume the personal use property referred to in question 5 was owned by the husband and the husband had received 40% of the income of the trust and was connected. If the property had been rented out but ceased, and the beneficiaries plan to move into it as a holiday property, would it be a personal use asset?

Question 7

- The share sale proceeds and the wife receive 100% of the income of the trust.

- Does the family trust need to add the value of premises three to calculating its net asset value?

- In respect of the sale of the shares in the company by the family trust, have one, of the two additional basic condition of S152-10(2) been met?

Question 8

- What would your answer be to the last question in 7, if the family trust had distributed 10% of its income and capital gain to the wife and a further percentage to the husband?

Question 9

- Is it possible for premises 1 and 2 to be active assets? What is the test?

Question 10

- If it is possible for the above to be so, and they are active assets, then – would the sale of the premises 1 in 5 years’ time possibly attract the concessions?

- Would the sale of premises 2 in 10 years’ time possibly attract the concessions?

12 Case study 1 – Answers

- The question is whether the company is in a business or hobby in the current year (the third year) being the year at disposal as a hobby is not a business, see TR 97/11, note if there is no business in the current year (disposal year), you cannot use the small business entity concessions.

- In respect of the second limb – test1 – which relates to the prior year turnover being less than $2M, you need to also confirm in respect of it being a business and not a hobby in this year. Note that the turnover of affiliates and persons connected with the company must be taken into account.

- In respect of the second limb – test 2 – you need to determine whether the aggregate turnover for the year is likely to be less than $2M. Arguably it is, as the turnover is small in year 1 and also only $800,000 when property is sold. A test to avoid as test 1 is applicable and the Commissioner may take a different view.

- In respect of the second limb – test 3 – clearly it is over $2M turnover. This gives credence to applying test 1 and less credence to the applicability of test 2. Arguable issue.

- Is the company an affiliate of the family trust (s328-130)? Trusts and partnerships cannot be affiliates of a taxpayer, however a trust or partnership may have an affiliate who is an individual or company. Arguably the company is an affiliate of the family trust as the family trust holds 100% of the shares in the company, and the company may act in accordance with the trustee’s directions or wishes or in concert with it.

Is the company connected with the family trust(s328-125(2))? As the family trust owns 40% or more of the shares in the company, and therefore income and capital and voting of the company, the entities are connected. - The active asset test will be satisfied if the Port Melbourne property was an active asset of the family trust for at least half the period of ownership of the property (s152-35).

Regarding whether the Port Melbourne property is an active asset (s152-40), it is an active asset at a time when it is used (or held ready for use) in the carrying on of a business by the familyBusiness trust, an affiliate of the family trust or a connected entity of the family trust. The company is a connected entity of the trust and it carries on a business.

The family trust owned the property for four years and it was used by the company in the course of carrying on its business for three years. Therefore, the active asset test is satisfied. - In respect of whether it would be the same if it was owned half by Finbar’s brother’s family trust, the company would still be both connected with the Finbar family trust and its use would make the property an active asset from the perspective of Finbar family trust. So, the Finbar family trust could apply the concessions to its capital gain.

Finbar’s brother’s family trust does not have an affiliation or connection with the company, so it would not satisfy the active asset test. - If the property was owned by Finbar’s wife, then she would be the relevant taxpayer (not the family trust) and you would need to assess whether the company is an affiliate or connected entity of the wife.

If the wife received 40% of the income of the family trust in the year of disposal, she would be connected to the family trust and the family trust would be connected to the company.

13 Case study 2 – Answers

Question 1

1.1. In accordance with s152-15 the taxpayer (i.e. the company) may satisfy the test if the net value of the CGT assets of itself, its affiliates and entities connected with its affiliates or connected with itself do not exceed $6 million. Therefore, first it is necessary to determine the net value of the company’s CGT assets.

1.2. If the net value of the company’s CGT assets is under $6 million, then it is necessary to determine whether there are any affiliates of the company and the net value of their CGT assets. Trusts cannot be affiliates (s328-130), so the trusts which own premises one and two are not affiliates of the company.

1.3. The wife of one of the principals who owns premises three will not be an affiliate of the company as she does not carry on a business. In order for the wife to be an affiliate of the company, she must act in accordance with the company’s directions or wishes, or in concert with the company, in relation to the affairs of her business (see section 328-130(1)).

Question 2

2.1. The next issue to determine is if the trusts are connected with the company. The company and the unit trust (which is the owner of premises one) are not connected directly, because neither has the required control percentage under s.328-125(2) in the other. The company and the unit trust could be connected with each other if they were both controlled by the same family trust shareholder and unitholder. If any one family trust owned more than 40% of the ordinary shares in the company and 40% of the ordinary units in the unit trust, then that family trust would control both the company and the unit trust.

The family trust (which is the owner of premises two) will be connected with the company if:

- The family trust has the required control percentage in the company which it does not; or

- The trustee of the family trust acts in accordance with the directions or wishes of the company and/or the company’s affiliates. This is unlikely to be satisfied.

2.2. The wife of one of the principals who owns premises three will be connected with the company if she indirectly controls the company under s.328-125(7). This may occur if the wife directly controls her family trust and if her family trust in turn controls the company by having the required control percentage. This does not happen here.

Question 3

3.1. Need to check net asset value, so maybe.

3.2. Yes, potentially, but you would carefully need to analyse each family trust’s position separately to determine affiliates and connected entities.

3.3. No. Trusts are never affiliates.

3.4. The unit trust (which owns premises one) may be connected with a family trust unitholder if the required control percentage is satisfied (i.e. one trust name more than 40% of the units). The family trusts cannot be connected with each other, because they are not controlled by the same third entity.

Question 4

4.1. The outstanding legal fees not rendered at the time of sale, can be take into account due to FCT-v-Byrne Qld Pty Ltd 2011 ATC 20-286.

It is arguable that the termination liabilities should also be counted. Note that if there was no contract before disposal, in my view, this would not be the case.

4.2. In respect of the earn-out there are two alternative ways to be assessed.

Under the current law TR 2007/D10 says the value of the earn-out right is added to the capital proceeds and maybe subject to the concessions. Any subsequent payment is not an active asset and could not access the small business concessions.

Under the proposed law, there is a look-through approach which means that they are able to attract the small business concessions. The ATO has allowed taxpayers to apply the proposed law, however if it is not eventually passed, you would need to amend these returns.

Under both methods the value of the earn-out would need to be considered.

Question 5

5.1. In respect of the loan accounts being deductible from the net asset value of that trust, they would be (see Montgomery Wools Pty Ltd) as long as the loan funds are related to a CGT asset of the trust (s. 152-20(1)) just before the CGT event. .

5.2. The loan liability would be taken into account, because it was used to acquire a CGT asset. Personal use assets of an individual are disregarded, but not personal use assets of a trust (s. 152-20(2)(b)).

Question 6

Assets of connected entities need to be added. Personal use assets of individuals do not. Whether it is a personal use asset will depend on the facts, see Altnot Pty Ltd v FCT [2013] AATA 140. If the property is not being used as a personal asset and there is only a plan to use it as a personal asset, then the asset will not be disregarded (s.152-20(2)(b)) and will be counted in the maximum net asset value test.

Question 7

7.1. If the wife is connected with the family trust (for example, because the trustee acts in accordance with her wishes or in one of the four years prior to the sale she received at least 40% of the income or capital of the trust), then the value of premises three would be taken into account in determining the family trust’s maximum net asset value test.

7.2. Yes. The additional basic condition is met as a CGT concession stakeholder in the company exists (the wife) and she has a small business participation percentage in the trust of at least 90%.

Question 8

The answer is no, unless the husband receives 80% or more of the income and capital of the trust.

The sale of the shares by the family trust would require one of the additional basic conditions under s152-10 (2) to be satisfied. As CGT concession stakeholders must be individuals, only paragraph (b) of the section is applicable, which requires that CGT concession stakeholders in the company have a small business participation percentage in the trust of at least 90%.

To be a CGT concession stakeholder in the company (s152-60) the husband would need to receive at least 20% of the capital and income or control 20% of the voting rights of the company (s152-65) after using the tracing provision. Further, if the trust distributed 90% of the income and capital to him, the test is met.

If the family trust had distributed 10% to the wife, the husband could have still received over 20% of the income and capital of the company after tracing (33% x 90%) so he is still a CGT concession stakeholder (s152-60), and also his wife would be. Further, the trust will have distributed over 90% (here 100%) to CGT concession stakeholder.

Question 9

The answer is no. To be an active asset, the trusts owning premises 1 and 2 must have the premises used by an affiliate or connected entity (s152-40). The company is not affiliated with the unit trust and is unlikely to be affiliated with the family trust which owns premises two (unless the trustee of the family trust exercises considerable influence over the company). The company would be connected with the unit trust if it they are controlled by the same family trust (for example, if one of the family trusts owns more than 40% of the ordinary shares in the company and more than 40% of the ordinary units in the unit trust), but this is not the case here 33.3%. The company would be connected with the family trust which owns premises two, if the family trust owns more than 40% of the ordinary shares in the company which is not the case here.

Question 10

There is no relevant small business entity in the year of disposal, so those concessions would not apply. The maximum net value asset test may apply if the active asset test is met. To satisfy the active asset test in respect of premises 1, the property must have been an active asset for at least half of the period of ownership, if it is owned for 15 years or less, which has occurred. The period begins when the property was acquired and ends when the active asset (the property) is sold. The sale of the property would still possibly attract the concession.

Premises two sale in 10 years time would also possibly attract the concessions, because the property has been used for at least 7.5 years by the company in conducting its business.

[email_link]